How Co-ops Raise Capital

An overview of funding sources for cooperative start-up and development

If you are starting or developing a cooperative, you have probably noticed that cooperatives do not use the same approach to capital raising that standard businesses do. The standard approach–selling a slice of a profitable business to investors–is not easily available for cooperatives. But, there are also capital-raising strategies available to cooperatives that are not available to standard profit corporations.

Cooperatives are democratically owned and governed by their members, and exist to serve their members by providing goods or services, helping members sell their goods or services, or providing a workplace for worker-members to provide service and receive wages. Cooperatives are a social business form. The cooperative form has more potential to heal social relationships and ecosystems than investor-owned business forms, because of the incentive structure and the way decisions are made. We will all benefit from the presence of more and bigger cooperatives. To create this growth, it is important that cooperatives receive adequate funding.

When any enterprise is getting started, it usually must raise start-up funding from multiple sources. Amounts from different sources add up to what is called a “capital stack.”

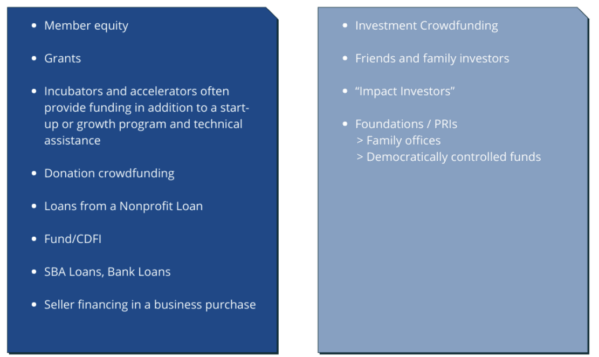

In a cooperative, the capital stack often looks like this:

*CDFI – community development financial institution.

Q: Where does capital for cooperatives come from?

Potential sources of capital for cooperatives include:

We often see some non-member investment in a capital stack. (The term “member” has a technical legal meaning, but in this blog post, “non-member” just means someone who does not use the cooperative’s services.) Non-member investors often provide a layer of funding that serves as the bridge between the initial member investment and an institutional loan. In certain cases, cooperatives have done larger private or public capital raises to meet their full funding needs.

Q: Why do cooperatives seek funding from non-member investors?

Members often cannot provide all of the necessary start-up capital themselves. They must rely on other sources before they can get a CDFI or bank loan. Sometimes these institutional lenders require a co-op to raise other capital first. Some types of cooperatives are small by nature, including most worker cooperatives. For this reason, members need help from outside capital that is friendly and patient.

Q: What can a cooperative offer to outside investors?

This is a difficult question for cooperatives because of the nature of doing business on a cooperative basis. Cooperatives exist to benefit members by doing business with those members. The goal in organizing a cooperative is to provide goods that were not already available in the market, or to help producers sell their goods and have more market access collectively than they would separately, or to operate a business through which members can provide services and receive wages. In general, the goal of a cooperative is to operate at cost, maintaining only a necessary reserve, and return all surplus to members. A cooperative’s goal is not to accumulate profit for itself or for investors. It is typically not seeking to be acquired by another company. This means cooperatives cannot approach capital-raising the same way that founder-owned businesses do.

However, many cooperatives can and do provide reasonable, non-extractive returns to investors. Cooperatives can be a meaningful way for “impact investors” to put their investment dollars to good use, and potentially receive a reasonable return on their investment.

At Cutting Edge, we regularly help cooperatives prepare capital campaigns. Here are a few types of investments that a cooperative can offer:

- Redeemable, non-voting preferred stock with a dividend that is a percentage of the original amount invested. Generally the investor will have to hold the stock until the cooperative has cash available to buy it back.

- Revenue-share debt or equity. In a revenue-share instrument, the cooperative will set a total repayment price, which is a multiple of the original investment amount (such as 1.5x–it generally does not need to be a high multiple for impact focused opportunities). Then the cooperative uses a specified portion of its top-line revenue to make payments to the investors over time. If the instrument is debt, those payments will be part interest and part repayment of principal. If the instrument is equity (stock), those payments will be part dividend, and part repurchase of the stock. When the full repayment amount is reached, the debt isrepaid, or the stock is repurchased. The variable that affects investor returns is the speed at which the enterprise can increase its revenue.

- Debt. Asking investors to lend, and promising repayment of principal with simple interest, is a good option for cooperatives who want to keep it simple. Before planning to take on debt, though, cooperatives should plan ahead and determine what later investments they will need. Debt on the balance sheet can deter later investors, especially institutional lenders, so we want to make sure the cooperative will have adequate equity before adding debt.

Q: If we have “outside investors,” is it still a cooperative?

Yes, as long as the members democratically govern the cooperative, and as long as the total design of the cooperative’s finances will primarily return surplus to members, in proportion to their use of the cooperative’s services.

All enterprises, including cooperatives, have to pay the cost of capital. For example, cooperatives can borrow from a bank and pay interest. The cost of interest takes away from the surplus that would otherwise be available for members as patronage dividends. However, the bank loan does not make the organization any less cooperative.

We can think of non-voting shareholders in a similar way. They may have approval rights over certain decisions that would affect them, such as dissolving the cooperative. But we always give preferred stock minimal or no voting rights–outside investors do not play any meaningful role in governance during normal operation. Preferred shareholders receive a dividend (when cash is available), but after that dividend is paid, the rest of the cooperative’s surplus can be returned to members. Some cooperative purists say that cooperatives should not have outside investors, but if a cooperative needs equity capital in order to succeed, we would like to see that equity capital come in, from supportive, non-voting investors.

Successful Examples:

Food Shed Co-op, a start-up food cooperative in Illinois, is in the middle of a capital raise now, and has reached over $1 Million of its $1.75 Million goal, in a combination of debt and non-voting equity. This raise will allow this cooperative to open a community-owned grocery store featuring local products.

Bay Area Ranchers’ Cooperative raised over $300,000 on WeFunder to build a mobile, rancher-owned, responsible meat harvesting facility, so that Northern California ranchers will no longer have to drive to the few, far-away processing facilities.

Switchgrass Spirits is a worker-owned distillery in St. Louis, Missouri. Early private investors supported the start-up phase by investing in non-voting equity and debt. Thanks in part to these early investors, spirits sales are now growing quickly.

If you would like help designing a capital raise for a cooperative, or if you have questions about cooperative formation, feel free to get in touch for a free consultation.